ql_rest is an experimental RESTful interface for QuantLib. This project aims to simplify the development of microservices for risk management and pricing various of financial instruments in the distributed environment in real-time.

ql_rest package includes conversion classes between JSON and QuantLibAddin/C++, Python classes to simplify serialization of JSON Objects to QuantLibAddin/C++, and Examples.

class qlVanillaSwap(JSONEncoder):

def __init__(self):

self.ObjectId = "";

self.PayerReceiver = "";

self.Nominal = 0.0;

self.FixSchedule = "";

self.FixedRate = 0.0;

self.FixDayCounter = "";

self.FloatingLegSchedule = "";

self.IborIndex = "";

self.Spread = 0.0;

self.FloatingLegDayCounter = "";

self.PaymentConvention = "";

self.Permanent = False;

self.Trigger = False;

self.Overwrite = False;

def default(self, o):

return o.__dict__

std::string vanillaswap::qlVanillaSwap(ptree const& pt)

{

return QuantLibAddinCpp::qlVanillaSwap(

pt.get<std::string>("ObjectId"),

pt.get<std::string>("PayerReceiver"),

pt.get<double>("Nominal"),

pt.get<std::string>("FixSchedule"),

pt.get<double>("FixedRate"),

pt.get<std::string>("FixDayCounter"),

pt.get<std::string>("FloatingLegSchedule"),

pt.get<std::string>("IborIndex"),

pt.get<double>("Spread"),

pt.get<std::string>("FloatingLegDayCounter"),

pt.get<std::string>("PaymentConvention"),

pt.get<bool>("Permanent"),

pt.get<bool>("Trigger"),

pt.get<bool>("Overwrite")

);

}

| Project | Version |

|---|---|

| Boost/Beast | 1.80 |

| QuantLib | 1.22 |

| ObjectHandler/GenSrc/QuantLibAddinCpp | 1.22 |

Basic Microservice is a set of helper classes designed to simplify the construction of basic micro-services. It includes a socket listener class, Quantlib pricing thread management class, and a producer-consumer queue to facilitate the communication between the socket session class and the pricing thread.

- The client connects to a microservice, submits a request via HTTP post, and receives back a token from the server(microservice).

- The server pushes request to the producer-consumer queue for the pricing thread to process.

- After some time, client connects to the server to check the status of the request by providing a specified in step-one token.

- If a request is still in pending, the client must repeat the step number there, until the request is processed by the pricing thread.

US Treasuries - https://ustreasuries.online

Python client posts market data and instrument term structures to two calculators. Calculators build a discount curve from the provided market data, price bonds, and make results available for client to retrieve. After 3 seconds, the client queries calculators by posting provided in step one token.

Libor Swaps https://swap.ustreasuries.online

ReactJS client publishes market data and term structures to a calculator and display results

Vanilla Options https://options.ustreasuries.online

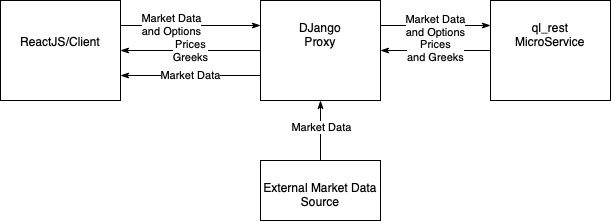

ReactJS front-end retrieves market data from the django server and posts results to a calculator through the same server that serves as a proxy.