[Archived] - Introducing a Sector Duration Multiplier for Longer Term Sector Commitment #421

Replies: 65 comments 249 replies

-

|

how do we avoid a pump and dump scenarios on the filecoin price with this?

there is not enough fil circulating to fully x5 the whole network. if we have one big enough player buying fil early and aggressively as soon as this is announced we might see unpleasant price movements that make it feasible to buy, extend, terminate i think

if this is a good idea - i do not know [edit] in fact that player wouldn't even need to actually extend - the FOMO this creates might be already enough |

Beta Was this translation helpful? Give feedback.

-

This is not a concern since the multipliers scale QAP. There's a QAP denominator in initial consensus pledge. Furthermore the pledge is multiplied by circulating supply. Both of these factors regulate the percentage of available supply locked. This provides an increase that is expected to saturate at the value we've pointed out around 50%. |

Beta Was this translation helpful? Give feedback.

-

|

@f8-ptrk rollout type shock is mitigated by several factors |

Beta Was this translation helpful? Give feedback.

-

|

@tmellan where have you been lately? Didn't someone give you the memo that there is a huge amount of FIL in the hands of a few people who initially participated in testnet and got all there FIL moved to mainnet? For them it is easy to instantly X10 all their sectors and push the smaller and mid sized miners out because they have that FIL available. The smaller miners don't have that FIL available. So what you are doing here is give them staking rewards on their FIL's payed by the smaller miners blockrewards who wil go /10 and who can't afford to X10 even if they want. |

Beta Was this translation helpful? Give feedback.

-

|

General point:

Concentration of tokens vs sufficient incentive to bootstrap project: standard perspective is early supporters get larger rewards and this is fair because they took early risk. This was before my time, others can comment on how close to optimal the design was.

|

Beta Was this translation helpful? Give feedback.

-

|

It does not matter if it was before your time or not. They did not take a bigger risk then others, thry got testnet (free) sectors converted to mainnet sectors with value. |

Beta Was this translation helpful? Give feedback.

-

|

will this change the min deal duration from 6 to 12 month too? if not - when is re-snapping planned so miners are not forced to keep "dead data" sectors proving (at least 6 month, 4.5 years in the worst case) just because it is more profitable than not doing so not everyone wants to store for 5 years and for most of the data out there it makes no sense to store them for long periods of time making long term commitments to keep sectors available, storage sealed shouldn't come with in flexibility in how data can be stored in these sectors. there is data out there that MUST be deleted after a certain period - re-snapping would give us a pseudo proof of deletion in some wired way |

Beta Was this translation helpful? Give feedback.

-

People don't have to do it for 5 years if they don't want to do it. |

Beta Was this translation helpful? Give feedback.

-

This is a good question but the answer might be something else which is the demand for using the network. See this funnel dashboard for Fil+, the network does not even have consistently more than 10PiB of Fil+ application everyday (and less than 1PiB of allocation/day). So the answer isn't just about the dynamic of CC vs Fil+. This FIP does not intend to change that dynamic between the two options. A key thing here is that Filecoin as an ecosystem might need more publicity, more eyeballs, more help, more resources, more applications to do more business development (and in more creative ways) to drive up storage demand. This FIP aims to help in that direction as well. |

Beta Was this translation helpful? Give feedback.

-

|

yes. those are the rules right now. 6 month to 18 month. now you put an incentive on doing it longer - what do you think will happen? it's called an INCENTIVE! if i do not do it i will loose out. you guys really that naive?

yes it is. but you have to ack that it might be a good idea to implement that first! you do not build buildings starting with the roof! this FIP is a lot. it's not something small. it's changing the protocol in a way you, SPs, no one has a clue what we will end up with. graph assumptions as you want - i am sure you did that before mainnet when the initial params were decided, and still: here we are - you plotting graphs again but this time ask people to trust in your assumptions, future predictions for 5 years... all i am asking for to not build your dream on sand but do the ground work first. |

Beta Was this translation helpful? Give feedback.

-

|

So then “keeping all things equal” it all comes down to whoever has access to the biggest amount of capital. This will surely increase price short term, but all normal miners and current healthy businesses without access to large sums of filecoin to lengten their CC x5 will be outcompeted. It is simple economics. Normal lifetime sectors will be heavily outcompeted by 5 year sectors. All average miners will cease to exist. Deals are still capped by bandwidth limitations of the overall network and large CC operations with no intention of storing data, but access to large amounts of FIL, will win. ONLY solution: cut back the multiplier tiers. Why 500% and not 200% ? |

Beta Was this translation helpful? Give feedback.

-

|

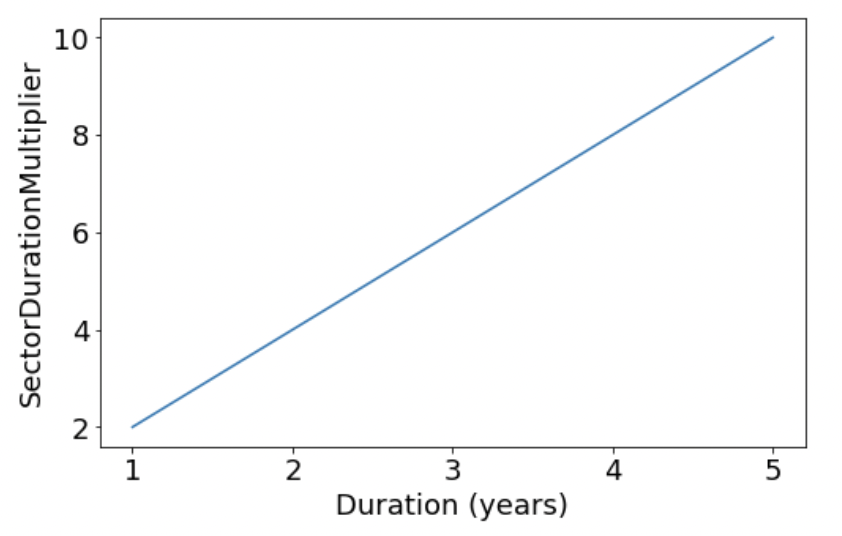

Long durations are good for the network but entail more risk. This needs to be rewarded to ensure a good distribution of sector durations all the way up to 5y. Even at the max of 5y (and there will be a distribution not absolute concentration at 5y), the reward is only half (5x) the extra incentive for useful data (10x). This seems fair given the extra risk to store for 5y, and the value that SPs doing this bring to the network. |

Beta Was this translation helpful? Give feedback.

-

|

Summary of Storage Provider questions and concerns raised in the EMEA SPWG meeting 1st August 2022.

Summary of CryptoEcon & PL comments:

|

Beta Was this translation helpful? Give feedback.

-

|

What now happens with FIL+ is that there is a HUGE cap on the availability due to healthy reasons such as:

This makes sure that no entity can simply outgrow someone with 10x because of their capital. If we push this proposal with an x5 on CC sectors we will go straight towards and proof of stake network and the most important factor of earning more and outcompeting the competition is having the largest bag of funds. |

Beta Was this translation helpful? Give feedback.

-

|

Also, commitment means nothing if you can terminate sectors for a small (90d) fee. Everything is liquid, also the sectors pledged for 5 years. We already saw this play out by the end of last year. |

Beta Was this translation helpful? Give feedback.

-

|

@tmellan can you please answer here on the remarks of @herrehesse . The smaller miners do not have access to unlimited funds where the bigger miners have. It is a known fact that they got their sectors beamed from testnet to mainnet by uncle scotty 2 years ago and b/c of that are sitting on huge amounts of FIL. As the same cake has to be divided ( rewards ) it simply means that the bigger miners who can X10 with more funds outcompete the smaller ones. They have only 1/10 th of their income left. Can you explain how this is healthy for decentralisation instead of repeating your own tune? Can you perhaps also tell us how this will attract new miners to join the space who need to start small? |

Beta Was this translation helpful? Give feedback.

-

|

Beta Was this translation helpful? Give feedback.

-

So I think centralisation is an important consideration we should think about in general and others should comment here too pls. But from my perspective, in this proposal, SPs have access to capital in proportion to their history of storage provision. This means there's no size bias in the proposal, in the sense that yes large SPs ofc have more tokens in absolute terms, but also more QAP to spread it over if they decide to boost to longer duration. Relative proportions and advantages/disadvantages remain the same.

It's easier to find collateral than scale operations which is likely good for small SPs. |

Beta Was this translation helpful? Give feedback.

-

|

I would like to propose a modification to the proposal, dealing with increased The current proposal increases the maximum sector commitment length from 1.5 to 5 years. It does it by increasing the ProposalThe core of the proposal is to separate the period of validity of a proof from the period of commitment for a sector. This leaves the 1.5-year sector extension process in place to maintain proof validity, but allows SPs to commit to longer periods. The existing sector A new sector property is introduced called

The proof refresh window creates a trade-off: the larger the window, the more refreshes can happen in a singular batch, but more frequently each proof must be refreshed. The proof expiration is not freely chosen by the SP, but takes a value that is derived and quantised from the sector’s activation epoch. Storage Provider can at any point call RefreshProofEpiration(SectorSelector) requesting a refreshed proof expiration. This call only results in an actual refresh of the ProofExpiration if called within ProofRefereshWindowof the ProofExpiration. In case of a PoRep bug, the It also has the following benefits:

Limitations of this mechanism include:

For more technical details please see this document. |

Beta Was this translation helpful? Give feedback.

-

|

Thanks @Kubuxu, I strongly support this as the implementation path for this change, over the naiive simple change to parameters. |

Beta Was this translation helpful? Give feedback.

-

|

Thanks @Kubuxu. We think this is largely separate to the central issue of the FIP, which, is whether and how we want Storage Providers to be able to express a long-term commitment to the network. This FIP seeks to be as straightforward of a change to address the problem motivation outlined. However, CEL would encourage and fully support your proposal as an additional FIP following this one (if accepted), as long as it does not change the core economics of the Sector Duration Multiplier Proposal. |

Beta Was this translation helpful? Give feedback.

-

|

Thanks @Kubuxu , This is generally a very good idea, not only attaching to this FIP, but generally a good structure for sector extension for long run. I would think this could be an independent FIP for PoRep security and deal/Sector extension. |

Beta Was this translation helpful? Give feedback.

-

|

@vkalghatgi The "straightforward" change to parameters introduces a very significant risk to the network. You can't invoke simplicity as an excuse for ignoring it. We can take discussion of the concrete implementation for this over to #415, but in my view the proposed mechanism is a pre-requisite to acceptance of the sector duration multiplier proposal. You could say that we would encourage and fully support your proposal as an additional FIP following #415 (if accepted), as long as it does not change the core storage security properties of the Filecoin network. |

Beta Was this translation helpful? Give feedback.

-

|

This is Hasan from DLTx |

Beta Was this translation helpful? Give feedback.

-

|

Hi Hasan, We're working on change to the proposal that can adapt the multiplier to be something SPs can better support, while still hitting of our key points: sufficient incentive that a large number of SP increase duration + increased and stable % of available supply locked. More details and supporting evidence incoming. On increasing the minimum duration by six months, the reasoning is threefold: Stability. A one year minimum smooths out locking dynamics by stretching inflow-outflow over a longer time period. Could I ask SPs to clarify their objections? Note, for sectors sealed right now, the average duration >> 6months, indicating most SPs will be unaffected. We need sample scenarios of showing the amount of FIL needed and awarded for different deal sizes and periods. This is the only way that we can all be on the same page and make the argument for approving or opposing the changes (edited to fix link) |

Beta Was this translation helpful? Give feedback.

-

|

you cannot get evidence for events in the future. by definition. all you can do is present educated guesses.

Yes you can. You present a solution - and you want to implement it NOW! ASAP!!! Not a "lets make this a string and not a []byte" change kind of solution but a "lets redefine core mechanics of the chain and change values we defined less than 2 years ago". But the problem this should solve is not clearly defined to most of the people. It would be nice if you could

this will help people understand where you are coming from. then we can start discussing the solution. for now it looks like you want to lock up more fil soon and fast for way longer times to an extent that will have consequences for SPs you seem to not fully understand. i know this would delay the process by at least a month or two or even more. SPs are most likely willing to take the "risk" of not implementing the solution any time soon but wait for you to fully explain why you want to do this and what the results of not doing it would be. btw: |

Beta Was this translation helpful? Give feedback.

-

|

the urgency is hard to understand. we all get the long term alignment incentive thing. |

Beta Was this translation helpful? Give feedback.

-

|

@tmellan , Do we have concrete proofs for the following reasoning? What's the other impacts? As a layer 1 design, we may want to provide more flexibilities instead of have more limitation. Increasing the minimum duration will absolutely reduce flexibility, and will push out some use case scenarios. More comments below.

Stability is more depending on decentralization and the scale of the network. This whole FIP may harm the decentralization since it will wash out small/medium storage providers; and also the scale of the network from infrastructure point of view since it moves to staking game model.

Are there any storage providers brings it up? A storage provider could choose one year if she does not want to "waste" resources resealing without any problem, but, anyway, there must be a reason for a SP to choose 6 months since she knows the cost is higher. Could we ignore that reason blindly?

Again, this is a free world people come and leave, we do not need to decide for people. A simple and flexible base would be fine. And, do not really understand why one-year minimum duration shows much stronger commitment to the long-term principles and long-term success of the network. What we know is that we are setting up a decentralized storage base and also a decentralized CDN. There are looooooots of data will be served in the network for a short period (6 months or less) in this fast-developing world, which we can not just ignore. |

Beta Was this translation helpful? Give feedback.

-

I commented on why I don't think this proposal implies more centralization here

L2s and HC subnets can be the wild west on top, but as the base L1 we need to maximize long-term stability imho

hmm, debatable

As a thought experiment, current min is 180d, do you think there should be no minimum at all? |

Beta Was this translation helpful? Give feedback.

-

|

Do we have modelling on the network QAP after this upgrade? |

Beta Was this translation helpful? Give feedback.

-

|

@jennijuju yep, renewal rate refers to sector extension. And yes, for sure, if @dkkapur has datacap projections that would be very useful. Thanks! To clarify, our current assumptions as follows:

These were copied from here. |

Beta Was this translation helpful? Give feedback.

-

|

@tmellan appreciate your patient response! will wait for @dkkapur or other folks from DP / fil+ team to confirm wthether |

Beta Was this translation helpful? Give feedback.

-

|

@jennijuju @tmellan -> DataCap will follow demand, not the other way around. If demand shows up to use the network and its provably useful to the notaries, then DataCap will be provisioned and created. For modeling impact of QAP, we should instead look at the growth rate of deals on chain + anticipated demand over time for Filecoin from the client/data owner side. I think 50% per year is too low for this given how small our current utilization is as a % of the capacity. In the last year alone, we've gone from <20 PiB QAP to <2 EiB QAP. That's 10000% increase. |

Beta Was this translation helpful? Give feedback.

-

|

On the data onboarding side, we've been playing around with different growth models and numbers. I'd suggest using something along the lines of 2%-7% growth WoW in data stored per day instead. cc @mr-spaghetti-code do you think this is still reasonable / in line with expectations we should set on demand growth? |

Beta Was this translation helpful? Give feedback.

-

|

Yes, I believe a target weekly growth rate of 2-7% is appropriate. Our deal pipeline is strong and we are primarily constrained by our onboarding rate (a function of tooling, transfer, and sealing rate). |

Beta Was this translation helpful? Give feedback.

-

|

I do not see any new SP's drawn to a place where they need to lock up x50 6FIL per TiB onto a harddrive to then sell that same storage for "free". This is not an healthy place to be in and we will become a staking protocol. Whoever has the most cash, wins. The reason why FIL+ works is because of a few things:

If you make it as easy as "lengthening a lifecycle" to get an x5, everyone who has the funds will do it because it is the easiest way to increase your block reward immediately. You say "great for long term commitment" and I say "everyone not able to compete will cease to exist". Hence no "decentralisation", isn't that why we are all here for? Do not mistake wishful thinking with simple economics: miners will be FORCED to get the x5 to stay competitive. Because of the decreased FIL/TiB revenue, miners who do not upgrade will go bankrupt. Small to medium sized miners need to lend more than 300%-500% of their initial Filecoin capital to stay competitive. No lender is capable of doing this. The rich will only out-grow all others, keeping equal hardware and not doing any deals. Please show me the maths and research on the following subjects:

I can keep going since I have another 50+ questions about this. But let's please continue this conversation as we all seek a beter future for the Filecoin network. |

Beta Was this translation helpful? Give feedback.

-

|

Hi @vkalghatgi , @tmellan , Thank you for the detailed FIP, but impacts are quite difficult to perceive, I’m a small individual miner true Filecoin believer, I quit my job for Filecoin, and I'm very worry about this FIP. I would like to highlight Two points that doesn't seem to be taken into consideration in the FIP. Time and effort

I think it’s unfair in regards to the effort these guys have done until now, and I would like to hear just one telling me that dealing with storage deals was not x10 more time consuming than pledging CC all day long; with the great work from the lotus team today even my cat 🐱 can do CC. LendersWith this FIP how can we survive without lenders ? If that the new rule, we can probably deal with it, but that should become part of the protocol and give any miners equal access to Fil, otherwise, this is just giving an extreme power to lenders and and unfair competitiveness to large entities. In a more general manner you present the macroeconomic aspects, I think many of us would like to understand what is going to be the individual impacts. It would be great if you could forecast the impact on some personas like :

Please ensure that FIP is fair for small players, and respectful for the time and effort they already invest, Long live to Filecoin 🚀 |

Beta Was this translation helpful? Give feedback.

-

@anorth may correct me if I'm wrong, however, if assuming #313 is finalized first or along with this fip, then that means, SPs who have been onboarding verified data, will be able to get both sector duration multiplier * fil+ multiplier upon sector extension. Reason being the fil+ multiplier will be lasting as long as the sector is still live. |

Beta Was this translation helpful? Give feedback.

-

Wanna flag this is untrue given the network protocol today, as the QAP will be adjusted according to the deal/sector spacetime upon sector extension. |

Beta Was this translation helpful? Give feedback.

-

|

@tmellan I think you have to review one of your assumption : 1/ as @jennijuju mentioned, when you extend a sector with verified deals, the Fil+ x10 is NOT extend. The x10 is related to the deals duration, not the sector duration. 2/ The network doesn’t support Deals extension => Deals have to be fully resealed when the deal expires 3/ SP doesn’t control deal extension, it’s a pure client decision. This 3 points show how it will be impossible for SPs with deals to keep their mining block rate after this FIP. Pikachu Mew2 Pikachu is the big looser here for having accepted deals : This will cost him : Time / Opex / Block reward You should find some ways to compensate that through the FIP or simply enable this FIP when the last deal is expired. |

Beta Was this translation helpful? Give feedback.

-

maybe #313 have to be a prerequisite of this fip |

Beta Was this translation helpful? Give feedback.

-

It will be possible, but not a done deal.

|

Beta Was this translation helpful? Give feedback.

-

|

Hello, everyone! I have compiled a list of concerns/questions presented during SPWG-CN meeting on August 3rd. Please note that these are taken on the fly by @Fatman13 which may or may not reflect what the speaker meant as things may get lost in translation or internet connection. Thank you!

|

Beta Was this translation helpful? Give feedback.

-

|

When do extension, let’s say for just a short time like a couple of days, will still be allowed after this FIP? And will initial pledge be calculated every time even for a short sector extension? |

Beta Was this translation helpful? Give feedback.

-

|

Hello everyone, for this, I put forward some of my personal views, welcome to discuss:

|

Beta Was this translation helpful? Give feedback.

-

|

I see some concerns about this FIP driving up token price (as new players wanting to seal 5y CC try to amass FIL for collateral), to a level where current SP's would not be able to afford collateral. While it is impossible to predict what will happen to Token price, and it is a fruitless effort to try to predict this accurately, let's follow the assumption from these concerns and see if they are justified. The implicit (and not unreasonable) assumption is that token price would rise (proportionately?) with network QAP (as more SP's compete to amass FIL). Ok so let's assume this. In this case the collateral that needs to be paid for a sector is also inversely proportional to network QAP, so the amount in fiat that needs to be paid remains constant. Also the amount of block reward that the SP receives, is inversely proportional to the network QAP. So while they will receive a smaller piece of the pie as network QAP grows, assuming token price increases also, then their block reward remains unchanged too in terms of fiat. |

Beta Was this translation helpful? Give feedback.

-

|

Let's also add another potential gamble. Lets say, as well as FIL price being proportional to network QAP, it is also inversely proportional available circulating supply, because of the concerns here that all the 5y CC sectors will snatch up all the FIL out there. This case is actually even more favorable to the current SP's (opposed to the previous example which was neutral). Collateral paid (at least the consensus pledge which is the much larger fraction) is also proportional to circulating supply, so less FIL will be paid, meaning no change to the amount paid in FIAT. Now, Block reward is not actually proportional to circulating supply, so FIL price is going up, and block reward stream remains unchanged, this means the reward is actually larger in fiat terms. Again, I am not betting this is what will happen to token price, I have no idea what will happen to token price. But it has been expressed that there is worry that FIL price will go up and this will be bad for SP's. I am saying IF FIL price goes up because of this FIP, that will be a net good thing for SP's. |

Beta Was this translation helpful? Give feedback.

-

|

quick question: slope 2 + 40% vs slope 1 + 50% and maybe lets do slope 0.25 and 80% in addition how do the pledge amount / 32gib curves look over time if we assume 10% of the non 5year sectors go to 5 years each month until we have the whole network 5year'ed |

Beta Was this translation helpful? Give feedback.

-

|

Can someone show me the actual calculations for SP's of various sizes and their expected growth and collateral requirements for 1x 2x 5x and 10x? I'd like to see the actual numbers in excel/sheets please. Before we can make any real assumptions about this proposal. Until then I think it is a huge gamble to go x5. |

Beta Was this translation helpful? Give feedback.

-

the earlier you do this the more FIL you need to lock up as the pledge will go down with the increased QAP. The later the less pledge you need but at a higher FIL price potentially. The overall rewards do not change - i am not sure if this is a net win for anyone in the end. As this is nto creating any utilization for FIl besides locking them up we will most likely see the same result in a few month after this FIP - price going back to where it is right now and all SPs spend a great amount of capital to go no where of course thats all just reading clouds, consulting the glass org, shaking the magic 9 ball....no one knows what will happen |

Beta Was this translation helpful? Give feedback.

-

|

Just following the guess that "FIL price may go up because of this FIP". My interpretation of that statement as I said could mean two things: Guess 1: FIL price goes up because it increases with network QAP. In this case this would be neutral to SP's, as their collateral and block reward are not changed in fiat terms. Guess 2: FIL price goes up because it increases as circulating supply decreases. In this case this would be a positive for SP's, as their collateral would not be changed, but their block reward would be greater than before in fiat terms. A million more things influence prices of things, so it is not the most useful conversation to have. But if the two above where the concerns, then I am saying those specific concerns should not be a problem for SP's |

Beta Was this translation helpful? Give feedback.

-

|

Attention! Hi everyone, Taking into account many of the points raised regarding SP preferences, we've adapted two key elements of the proposal:

In addition, several points have come up repeatedly, and we attempt to address why we think these will not cause problems. The document is here: Thanks to all who can take the time to read, and especially those who can take the time to comment. This is a critical feedback loop for us. Pending community response, we'd like to include these changes to the current FIP draft. To help direct, please 👍 or 👎 to this post. Thanks all. cc @zixuanzh @vkalghatgi @anorth @jbenet @momack2 @Fatman13 @Kubuxu @f8-ptrk @kaitlin-beegle @geoff-vball @AxCortesCubero @misilva73 @jennijuju |

Beta Was this translation helpful? Give feedback.

-

i think this is a very extreme, defensive speculation. And I hope the community would have some trust in core devs, have the best interests on “what will make network more useful and being more value to the network” in heart. |

Beta Was this translation helpful? Give feedback.

-

|

@jennijuju I am not doubting any of the hard work this team has done, and I am also very supportive of the proposal. But some really important calculations and effects have not been thought through properly. And some things feel rushed or odd. This has nothing to do with "being rude". We are all adults and can take a hit or two, don't you think some storage providers feel awful right now because of this proposal? Continue the conversation, my point remains the same, I believe x5 is a to high factor and the negative network effects will not be pleasant. I believe that x2 is more than high enough. Problem is I have not seen calculations for either of them, only formula's. If someone can concretely give me an example, from a SP perspective, on why x5 is needed I might change my opinion. |

Beta Was this translation helpful? Give feedback.

-

Yes, all feelings are valid and fully ack! |

Beta Was this translation helpful? Give feedback.

-

100% no to the mechanism, introducing a sector duration multiplier, whatever the slope is. |

Beta Was this translation helpful? Give feedback.

-

|

You're right. This proposal is very hasty and does not take into account the actual situation of most storage providers. Therefore, I suggest that the storage providers be cut off as leeks. |

Beta Was this translation helpful? Give feedback.

-

|

I have an idea, If you really think circulation is a big problem and have to deal with immediately, instead of trying to find tons of reason to convince the SPs to be the only one to bear the cost, why doesn’t PL or the foundation burn some tokens they control just like CZ does for BNB? It seems like a least destructive nor controversial way to achieve the goal, you don’t even need a FIP and can do it immediately, problem solved! |

Beta Was this translation helpful? Give feedback.

-

|

or we extend the vesting schedules of ICO tokens by 500-100% - show some long term commitment!!! edit to add [edit] |

Beta Was this translation helpful? Give feedback.

-

Absolutely, that will work too. |

Beta Was this translation helpful? Give feedback.

-

|

You're right. This is a good suggestion. You should let Hu Pang know. |

Beta Was this translation helpful? Give feedback.

-

|

Can someone explain to me with corresponding calculations why we can not do a 2x for a 5 year sector? |

Beta Was this translation helpful? Give feedback.

-

|

This is the direction what I can imagine... and initial pladge will not need to change |

Beta Was this translation helpful? Give feedback.

-

|

It feels to me like a LOT of worries and arguments are not listened to. Is there a list online where all of the arguments are stated? Love to see this, and if not I will make it myself and share it. 2/3rd of the community vote also sound reasonable for this proposal. Will this proposal be pushed whatever the feedback from the active community? I do need an answer on this because then I can prepare for it. Right now it seems most active and knowledgeable data onboarders and SPs are against the current form, but with vague and evasive answers it seems to me that it will be implemented regardless. Would be appreciated if we know what our voices are “worth”. |

Beta Was this translation helpful? Give feedback.

-

|

@herrehesse ppl are listening and giving answers:

And for sure, a few more things need more detail --- clarifications on porep security, deal extension and lending --- but ppl are very actively aware of this, and to be clear SPs are absolutely being listened to. |

Beta Was this translation helpful? Give feedback.

-

|

So, if everyone is listening to SP concerns, is it now finally clear that we do NOT want this in its current form? |

Beta Was this translation helpful? Give feedback.

-

|

Have been getting questions and wanna leave a quick comment If an existing deal renewal or extension is necessary for this FIP, then please add that as a prerequisite to this FIP. And some core devs might prioritize coming up with a proper solution for that first. |

Beta Was this translation helpful? Give feedback.

-

|

We’re a Sydney based SP with 25PiB of proven capacity in the Filecoin network, as such we’re motivated to support activity that will boost the price of FIL and reduce volatility. Having said this, we are vehemently opposed to the artificial manipulation of FIL supply designed entirely to boost the price of FIL for the benefit of a select few significant holders of supply. The price manipulation is a short term fix to long term problem and we’d much rather PL focus their efforts on increasing demand for FIL by onboarding meaningful customers and improving the customer utility, stability and retrievability. The proposed FIP does: The proposed FIP does NOT: A 5 year FIL+ sector requires 50x the amount of capital to collateralise that sector (compared to a 1 year CC sector), where do you expect SPs to produce that amount of capital if they want to remain competitive? |

Beta Was this translation helpful? Give feedback.

-

|

As a small SP with 4PiB adjusted storage power, I don't have much additional capital for 50x collateral. I even couldn't get any FIL loan now. |

Beta Was this translation helpful? Give feedback.

-

|

As a non-SP, I'm for this FIP in principle but from what I understand / am hearing from folks on this thread I'm concerned about moving forward. Reading through a lot of other folks' concerns - a few things stick out (maybe these have been addressed, but it's honestly hard to keep track with this thread):

This strikes me as very weird reasoning. It's either the case: In both cases, timing of upgrades seems like an explicitly bad reason to try and push this forward - as its the importance of this FIP that will dictate on whether it eventually is accepted by the community. Given the state of the discussion, it seems there are many folks in the community who feel strongly against (not even the idea itself, just the current timing / incarnation) - and its not obvious all the concerns have good answers (see below).

Many of the lending programs today are limited in scale in terms of SPs they can concurrently support, and tend to target SPs who can accept large volumes of FIL (someone correct me if this is wrong!). This means the average smaller SP will not have access to capital to grow at the same rate as the larger SPs. I know there are a number of teams working on liquid staking like programs when the FVM launches (which hopefully will serve a broader range of SPs) - but until that's a reality, we're exacerbating a divide which will only worsen diversity on the network. At least for me, it feels like this is a clear issue with the FIP as it stands - and one that requires no modeling or theory. It is practically the case that there are not lending options accessible to all SPs - and until thats remedied making this sort of change will have a perverse effect on SP diversity. (Even if there were a new lender to appear who would work with every SP it also seems concerning that everyone would need to set up a multisig for owner accounts and the potential risk that might incur to the network. EDIT: been poitned to FIP29 as a potential answer on this point, though idk if any loan programs use it) Is there a reason then to implement this FIP before the FVM / permissionless lending markets are live? Am I missing some context here which should change the reasoning above? |

Beta Was this translation helpful? Give feedback.

-

@tmellan , are you talking about security issue by saying So we've gotta be serious? Is this change trying to solve this "serious" issue? And, there are two things you may want to think about:

|

Beta Was this translation helpful? Give feedback.

-

|

@DecentCr8 No, I wasn’t talking about security/bug or anything like that

Yes, agree

Sorry I don't follow, maybe rephrase?

Yes, for existing and future participants, in FIL-on-FIL ROI terms. The cost of the change is not getting 80% FIL-on-FIL ROI. But there are benefits, which we've tried to set out as clearly as possible. The way I see it there's 3 choices:

|

Beta Was this translation helpful? Give feedback.

-

There’s very limited corporation( 2-3 ) that can provide loans longer than 360 days and only changeowner to them. But You still need do a lot of KYC work and a long time to complete the loan. Which of course if you're a small SP, and you even don't have a corporation and staff to do that, it will not be a simple task. With other corporaion, you need to pledge your hardware and even put your hardware in their datacenter. Or the time is too short even to seal 210 days sector. The interest will be 20%-30% now, and if the FIP is implemented, the Miner annualized income will be 20% as this one pointed:#421 (comment) In this situation, the loan from corporation interest must be lower than 5% (1/4 of block reward maybe) , which of course is Negative incentive for the corporaion. A lot of guys think DIFI will help, i think it well, but we still need to see

As i know, the largest DeFi of FIlecoin only get 1.5M staked in ethereum before. That's really not enough. |

Beta Was this translation helpful? Give feedback.

-

|

To address a few points above:

Fwiw, I've been advising some teams working on solutions for the FVM in this space, and I think the state of lending will get substantially better once the FVM ships (don't want to out anyone who is in stealth mode - but the technical designs feel substantially friendlier on both sides). Fwiw - I'm generally bearish that we will be able to lean on DeFi in other ecosystems to solve our capital efficiency problems (just as a matter of how complicated the solutions tend to be and the risks involved).

In general, I think folks will demand a higher ROI (in FIL terms) if they're incurring higher risk - but to @tmellan 's credit, if we can smooth out the waves of expirations (so it isn't an overhang on the FIL economy every couple quarters) this may be offset in general improvement. I guess the impt point here is most folks looking to stake I don't think purely denominate their ROI in FIL on FIL returns - its also a function of FIL/Base currency (whether thats USD, ETH, BTC, you name it). If FIL/Base is steadily chugging upwards, folks are likely to accept a lower yield (ETH as an example is targeting single digit yield, and folks are generally ok with this as theyre not thinking in purely eth on eth terms.). One slight advantage we have (vs some other protocols) is that there are different profiles of folks who might be staking on FIL - rather than just having folks who are locking FIL who are long the network, you could imagine tokenized representations of debt being used in a number of contexts:

The DataDAO use case is an interesting one - where if the DAO is looking simply to index on FIL inflation, they aren't just looking for the maximum reward, they're looking for stable returns for their endowment to fund ongoing storage (https://twitter.com/jnthnvctr/status/1545401176392437762). I have more thoughts on this (but also don't want to out some early ideas on the DeFi side). NFT Storage is looking to eventually DAO-ify (and hopefully lay blueprints for other DataDAOs and contracts that can be used) to enable the above use case.

I think for everyone to be able to evaluate things with clear eyes, there is base level of shared context we need to reach. Personally, I was unaware of the upcoming wave of sector expiries - and I'd be curious how others see this problem. Pulling together many threads, it feels like a few things are true:

I think without having a shared understanding of the world, it's hard to draw meaningful conclusions (for me as just a contributor, for SPs knowing their own operations) about what makes sense.

One note I'd make is that the proposals you laid out @tmellan are not the only ones that need to be on the table. I think if other SPs appreciate / agree that the macro env is going to be painful, its reasonable to pursue something shorter term to hit the n17 upgrade. But the alternative doesn't need to be a year from now - it could also be the Feb update no? Imho one of the biggest things we've heard in this thread is trying to tie this with permissionless lending markets (see 1475's post at hte bottom). |

Beta Was this translation helpful? Give feedback.

-

yes, i think defi and other staking stuff shall be better than this FIP. Find the new use case. |

Beta Was this translation helpful? Give feedback.

-

|

I’d like to present my summary evaluation of this proposal as it stands today (partially in response to @Fatman13's request, partly to agitate for action). I am not a member of the CEL team or an author of the proposal, but highly motivated to realise a robust, useful, and growing Filecoin network. This is my opinion, though I have drawn some ideas from the discussion here. I disclose that I am also a FIP editor (an administrative role), but here I am wearing only the hat of community member and core dev. I think something like this proposal would be good for the network, and I’d like to see it implemented. But the current form has a number of specific issues that, in my opinion, must be addressed before we can be confident it is a safe, beneficial, and equitable change to make. The right goals & directionally good mechanismsThe proposal is well intentioned. I understand the primary goals to be improving the stability of the storage commitments underlying the network as well as the stability and predictability of storage provider returns. I think these are good goals[1]. It aims to do so by allowing longer-term commitments to storage, allocating a greater share of the block reward stream to those longer commitments, and adjusting the pledge lock target upwards to bring balance to supply flows. There is also an ethos argument that the network should skew rewards towards longer term commitments. I am reasonably convinced that these mechanisms will achieve the goals. [1] What is the tradeoff for these goals? It’s a bit implicit, but greater stability will come at the expense of absolute commitments. The goals prefer to lower variance and accept a slightly lower total commitment than otherwise. The network will deny SPs optionality for short sector lifetimes, which makes committed storage slightly less valuable to them in aggregate, and so they’ll commit less of it. The most marginal (i.e. least stable) SPs will cease to participate. I think this is a fine tradeoff for the network to make, given the current 18EiB storage commitment. In the long term, stability will lead to greater aggregate utility. Major issuesThe following are major issues with the current proposal. Each one of them is a blocking issue to my support. However, I think all of them could be addressed. If they were, I think this the proposal would present clear benefits with reasonable risks. Pre-commit deposit risk modellingThe proposal notes that PCD will increase in line with the maximum potential lifetime reward of a sector. Merely noting this is not sufficient. We need to see an analysis of expected returns given assumptions about prove-commit failure rate: perhaps the observed network-wide rate, and some multiple of that for an individual SP’s risk model. The risk is aggravated by batching, which is necessary for high-throughput or high-base-fee onboarding. It is not clear to me that lower-quality sectors (CC or short-duration) are even above FIL-on-FIL water, here, or at what point batching becomes untenable. Action: SP return projections must take this into account. It’s possible that a compensating mechanism will be required to keep CC and batching viable. PoRep security impactThis proposal increases the maximum sector commitment to 5 years, which breaks the existing (somewhat implicit) security policy and mechanism for a fault in PoRep. The FIP notes this but does not propose a mitigation or state that its implementation should be conditional one. The FIP authors have attempted to dismiss this issue as being a separate issue and not coupled to their proposal. In my view, a policy and mechanism to address potential PoRep flaws is a pre-requisite to breaking our existing one. @Kubuxu and I have spent some time trying to design a mechanism that could decouple the validity duration of a proof from the commitment duration of a sector. We hope to contribute this in order to unblock the sector duration multiplier proposal. The FIP should state this as a prerequisite. See #415 Action: The FIP should state the pre-requisite and authors should contribute to the policy analysis. Inequality of access for existing sectors with FIL+ dealsThe proposed mechanism is agnostic to deals, but current limits on capability of the built-in deal market mean that, for existing sectors, those already hosting verified deals can't be extended immediately to fully exploit the multiplier, while CC sectors can. The raw byte power attributable to the sector could be multiplied, but the FIL+ boosted power would be countered by the QA power’s “spreading out” effective. This means existing CC sectors can increase their proportion of total power and hence rewards by some multiple. Assuming any significant uptake of extension of CC sectors, the share of per-sector reward to existing FIL+ sectors could fall significantly faster than without this proposal. This issue applies only to existing sectors, not new ones. But of course existing sectors account for 100% of committed storage provider participants. The problem is the inflexibility of existing deals, so the proposal being agnostic to deals has real implications. This problem goes away in 1.5y when all such deals have expired. I am working on some improvements to the flexibility of FIL+ datacap and deals, but even if they land simultaneously, I am not confident they adequately address the issue. Most likely, extension of existing FIL+ deals would be at client discretion and require action and (small) cost on their part. SPs would experience divergent outcomes depending on their luck of their specific clients. I could be convinced otherwise by evidence that clients representing, say, ¾ of current verified deal bytes stand ready and willing to extend their deals when possible, or SPs clearly confident of that. Or a FIL+ notary vote that they will mint new datacap to extend any and all existing deals. I think the option of awarding duration multipliers only to newly-sealed sectors should be investigated more thoroughly. Even with that restriction, the future rewards of existing FIL+ sectors would fall, but at least their providers would be on equal footing to seal more, high-multiple sectors. Ramping the maximum duration very slowly (18m) could also reduce the impact (because the old deals will expire). I would love to see other ideas to restore equality. I’m aware the CEL team’s position is to advocate for applying the multiplier at extension because to apply it only to new sectors “risks us seeing much smaller positive effects” and “will be an incentive to let sectors expire” (… in order to seal and commit new ones). I don’t find this convincing, and certainly not more powerful than the inequality against the network’s most utility-aligned SPs. Especially since more muted effects would reduce the risk of many uncertainties and shortcomings, and I’ve seen no modelling. In short, I don’t think they tried to make the idea work because they haven’t been forced to. Action: Authors should model and publish the best possible version of a change that applies only to new sectors. Show analysis for early-termination incentives, and propose mechanisms to mitigate them. Pretend it were against the law to change the policy for existing sectors: what’s the best you can do? Support for FIP-0045 ([draft](#432)) is also welcome. The FIP also needs to fix simple policy numbers like max deal duration ShortcomingsThe following are significant shortcomings or weaknesses that I would like to see addressed, but don’t quite rise to the level of a blocking issue to me. They are risks that I am unhappy about. Uncertain short-term dynamicsThe proposal appears to prompt an immediate drop in per-sector profitability-on-pledge (according to published charts), and there’s also some incentive to delay extending sectors until the pledge-per-QAP requirement falls. There may also be an incentive to terminate the oldest existing sectors to re-use the pledge for new commitments that gain a greater return on hardware cost (but lower return-on-pledge?). These all point towards a short-term drop in onboarding rate or even total power. (My guess is that this is more likely than a rapid increase in QA power, but see “Rollout shock” for that one). Some of these dynamics might counter each other, and other system properties may also act as negative feedback, but I haven’t seen any attempt at dynamical system modelling to understand the instabilities, feedback loops etc, that might be in play. I’m willing to take the long term projections as given, but in a system like this with reflexive dynamics on token price, the long term could be seriously undermined by a short term feedback loop. A 3-6 month ramp on the maximum sector duration/multiplier could significantly mute any unpredicted dynamics. Denying multiplier on extension of existing sectors would also constrain any such effects. Or I’d welcome other solutions. Action: Analyse and show best version of a ramp on the multiplier. Analyse and show best version of applying only to new sectors. Show dynamic modelling to demonstrate self-healing behaviour without other mitigations. Rollout shockIf CC sector extensions can enjoy full multiplier, there is a positive feedback loop for one or more large SPs attempting to gain a dramatic increase in power. A provider/consortium that did have the capital could pack blocks with extensions and censor extensions of other providers. If they gain any momentum, their increased power would increase the rate at which they could pack blocks and the effectiveness of censoring others: a positive feedback loop that increases the effectiveness of their attack. This is independent of the consensus risk analysed and noted below. I think this scenario is less likely than the one above in which onboarding decreases, but “less likely” isn’t an appropriate level of assurance for a billion-dollar blockchain. Rollout shock would be effectively prevented by a ramp on the maximum sector duration/multiplier. Or I’d welcome other solutions. Action: Analyse and show best version of a ramp on multiplier. Develop alternative solutions to consensus risk due to rollout shock. Moving towards proof-of-stake securityThis proposal shifts the basis for consensus power sharply towards money rather than physical storage. I am not comfortable that PoS networks are sufficiently validated as a secure foundation for trustless collaboration (although eagerly await learnings over the next few years as Ethereum and other networks mature). This seems to be an unintentional side-effect of the proposal; it’s certainly not stated as a goal nor invited as a topic for discussion. I wish there were proposals for ways to achieve the goals of stability and predictability without relying so much on stake.

Underestimating a complex adaptive systemFilecoin is a complex adaptive system. It is not generally possible to predict the effect of some changes to the system, because second- or third-order effects might dominate and agents will change their behaviour in response to a changing environment. There is non-trivial risk that the system has been mis-characterised. Changes aimed at stability could end up reducing network stability, or increasing fragility. Perhaps the storage commitments will be more stable, but the system more vulnerable to external shocks? Perhaps stable profits will deceive SPs, and they’ll take less risk-mitigation measures as a result? How would a major SP failure affect the network perception? How does this compare with a simple POW system, which is less stable but more anti-fragile? We can’t predict these, and the authors have stayed clear of predicting any outcomes (see uncertain system dynamics and rollout shock, above). But working with such a system requires a “probe, sense, respond” engagement rather than a “sense, analyze, respond” approach that would suit a complicated but predictable system. This proposal seems like a significant step change based on a belief that the system is understandable. There is some risk of an adverse outcome. The authors have justified the large step change with (paraphrasing) “SPs need stability, we don’t want to change often”, but also downplayed with risk with “we can change it later if it doesn’t work out”. Pick one. A more incremental approach, or at least a ramped rollout, could help buffer us from getting it wrong. Nevertheless, I don’t consider this a blocking issue, just a pre-mortem. Buying an expensive optionThis proposal achieves stability by inducing SPs to make longer commitments. The network essentially pays the SP a premium to give up the option of dropping a sector. (The SP can pay termination fee to buy the option back). 5x reward seems like a very expensive option. We don’t know whether this scale of incentive is necessary to shift the average commitment duration higher (i.e what the right price for the option is). The authors have offered no analysis of multiplier slopes below 1.0 so the community have no ability to compare the projected outcomes. The one-shot nature leaves little scope for “price” discovery. The size and step-nature of the change introduce many of the risks above. I don’t consider this blocking, just an unfortunate over-payment. Weak justification for raising minimum sector durationThe proposal raise the minimum sector commitment from 6 months to 1 year. While it does align with the goals, there’s no evidence it’s necessary after introducing a massive incentive to longer durations. The only argument for this that I think holds any water is the ethos one: “because we think it’s right”. Arguments that sectors expiring every six months need to find new sealing power to compensate are flawed: a 6-month sector can be extended without resealing. Arguments about client demand are similarly orthogonal to the issue. I don’t consider this blocking, just unnecessary rules that exclude a market segment. Missing concrete numbers for pledge, reward, etcSPs have requested concrete numbers for the pledge, day reward etc derived from the network conditions today. The proposal should show the current values, and the values immediately after the proposal was adopted, and, if relevant, the range of values as they would change in the future. This is a reasonable request from SPs which should be answered. The PCD values are already given. Action: Give actual numbers in the FIP Closed-source modelling and simulationThe FIP authors have presented some analysis documents, including charts of projections and simulations. They have not provided the code for these models so no-one in the community can check their correctness, or use them to answer questions other than the ones that the authors wish to publish. The authors are understandably reluctant to present projections that have anything to do with token price, but others can use their code to make their own. The source code for and data inputs to analysis should be provided to network participants to verify. Preferably checked into the FIPs repo. Resolved or non-issuesThe following are issues that have been brought up, but I think are adequately addressed already.

|

Beta Was this translation helpful? Give feedback.

-

|

Thank you for the clear write up! 💙 |

Beta Was this translation helpful? Give feedback.

-

|

@anorth. This is extremely helpful. Thank you so much. |

Beta Was this translation helpful? Give feedback.

-

|

How is "financial capital" easier to come by than any other capital? Equipment finance is a far more liquid market with significantly lower cost of capital, hardware can be financed over 5 years at 5%... this is the easy part. Borrowing FIL requires collateralisation and greater than 20% cost of capital with earnings locked up for 6 months. This is not a "Resolved or non-issue" the fact that this concern has been dismissed means that you have absolutely no idea how financial markets or SP businesses operate and I have zero confidence in the assumptions behind this FIP. Raising capital for the purpose of buying FIL on balance sheet in the current climate is extremely difficult, the last time we did that 95% of this value got wiped out, try explaining to an investor why this is a good idea to do it again. |

Beta Was this translation helpful? Give feedback.

-

|

Arock supports the FIP. We believe that it benifits the Filecoin ecosystem. The FIP is not forcing Fil miners to stake/pledge more FIL, just an option to do so, and it is rewarding miners that are locked in for a longer period. But we should adjust the rewarding system to scale according to amount of stake and duration of the sector, with a proper formula, rather than a fixed multiplier. FIL+ locking period is not decided by miners, data providers will define how long it should be stored. With the multiplier, there will be more long term real data storage demand, more LDN application, less notary collusion. From my personal point of view, this proposal should be approved as early as possible but implemented after the FVM upgrading. We expect that there will be some DeFI dapps on chain once it is supported, for FIL holders to lend, and for miners to borrow FIL to pledge, with an open interest rate for everyone to calculate and make decision. It could also benifit the actual network utilization. FVM upgrading, retrieval, CDN market and other development in near future need a stable network and FIL price. Less token circulation in current market situation will be more friendly for user adoption. |

Beta Was this translation helpful? Give feedback.

-

|

Sharing a conversation I had with SPs. I'm not a SP. I am just a community member, who is 100% devoted to the growth of Filecoin.

|

Beta Was this translation helpful? Give feedback.

-

|

We open sourced our model here (https://github.com/lyswifter/FIP36_simulation-mild_growth_assumption) to simulate Filecoin network dynamics post FIP36, specificly what’s the SP’s ROI looks like at any time of points in next 6 years by assuming The ROI doesn’t include operation and hardware costs, nor gas fees because that’s variant SP by SP, it’s just fil based return, concretely, 365 days of block reward divides pledge, you need to dedicate the gas fee, collateral and fiat cost from the aggregated block reward by yourself based on your own cost structure. In short, you might see much lower ROI in your real business operation than the model tells you. This model is written by python Jupiter notebook, if you don’t have experience but still want to try it, you can download Anaconda and use “jupyter notebook” command to start it, and you will find tons of online guides to make the learning curve not intimidate at all. Caveat! This notebook should not be viewed as financial decisions by any means, there might be defects of simulating Filecoin consensus or false assumptions of network parameters and etc. Although it’s worth to mention that with two months of emulation from Jun 17 to Aug 22, it’s pretty close between the model output and network data (block rewards and circulation). Again, you are free to modify any part of the model, especially the part in “## Assumptions we can modify” code block, and re-run the notebook to check how that impact SP’s ROI. By changing these assumptions and compare the results, we have observations as below: 1, SP ROI will continue to drop and will be in below 20% fil based APY range after FIP36 Since this APY is only about (block reward)/pledge, so with 20% to 30% fil-based APY SP will enter “bleeding zone”), assuming in real operation, SP still need to deduce the cost of collateral(30%ish loaning rate at this moment) cost of gas (0.6% of pledge for 50x sector to 30% of pledge for 1X sector), hardware and datacenter cost, fixed cost (team, network, etc) Based on above 4 observations, we infer that Advise: If you see any discrepancies between this model and the Filecoin consensus, or suggestions to improve the model, please let me know. |

Beta Was this translation helpful? Give feedback.

-

i don't know. The whole FIP is not decided now. And it seems the key point is whether the previous sector will be multiplier. |

Beta Was this translation helpful? Give feedback.

-

|

I am trying to go through your code to understand your calculation and how it differs from other models. I have one significant objection to this model, which is this doesn’t really seem to be simulating anything about the duration multiplier itself. It seems just a simulation based on different raw and QA power growth rates assumptions, that seems mostly unrelated to this FIP. In particular it seems the only way you are modeling the effects of this FIP is by assuming that after the duration multiplier comes online, you assume there will be a significant drop in network raw power growth rate. And then you use as input; some decreasing growth rates at different points in time after the multiplier comes online, and make some also pessimistic assumptions about the network QAP growth. The current simulation seems to be just answering the question “what happens to SP ROI if there is a drop in network power growth?”. I think this would be even a fine assumption if you have some explainable argument or mechanism that shows implementation of duration multiplier leads to decrease in network drop. Instead this pessimistic outcome which is presented as a conclusion which emerges from some simulation, in fact is not a conclusion, but an assumption built into the simulation. So to be clear what I think you are presenting is “If there is a significant slow down of network power growth, this would be bad for ROI”, what you left out is a justification of how this relates to FIP 0036, unless there is some other simulation that shows that the effects of FIP 0036 would lead to such a power slow down. I would recommend others to also consider the ROI calculator built by starboard (https://observablehq.com/@starboard/sproi-fip-duration-v2) which is also open sourced and you are free to explore the code. I believe here the effects of a duration multiplier are actually examined. First this model needs an assumption of raw power growth (which you can tune, optimistically, pessimistically or neutral). Then the duration multiplier comes in in two ways: user can input a prediction of what they think the average sector duration would be (if you think everyone will go ahead and get the maximum multiplier, or not). This average sector duration controls in the simulation what the total network QAP will be given the total network raw power assumption, and also average sector duration affects the expiration rates used to calculate circulating supply. Is it a perfect simulation with all possible effects taken into account? probably not, but it is one with clearly stated assumptions and limitations. |

Beta Was this translation helpful? Give feedback.

-

|

Thanks for raising the questions @AxCortesCubero. About the duration multiplier from the FIP, my view is this is just a lever for SPs to choose how they want to allocate their capitals between hardware investment (represented by raw bytes power) and token investment. Therefore 1, My ROI is calculated by (365 days aggregated block reward) divides pledge, so duration multiplier has no impact in this calculation what so ever. For example, if one SP sealed 3 CC sectors for 1 year each, and another sealed 1 CC sector for 3 years, they have the same fil-based ROI as pledge and block rewards will be all the same, given they sealed at the same time of point. 2, About raw bytes growth after the FIP, my assumption is, all business operators want to optimize their cost structure, given my example above, 3 CC sectors 1 year each definitely requires higher hardware cost than 1 three years CC sector, though the token return is the same, so a nature choice from SP will be committing as little raw bytes as possible will be a far more efficient way of spending capital , but again, that’s only represent my view, and maybe some other community members who view this change as a “POW to POS change”, if you disagree with this assumption, you can state why and tuned the raw bytes growth parameters |

Beta Was this translation helpful? Give feedback.

-

|

I think it is fine for everyone to have their own opinions about what they think the impact of this FIP would be on storage power growth. The important thing I think is to make sure it is clear that this is an assumption you built into your simulation, stemming from your heuristic analysis, and not an outcome or conclusion that emerged from your simulation. That said we could also now discuss your assumption instead, which I think has some issues. First you state the duration multiplier has no effect on your definition of ROI. This is strictly true in a far future equilibrium sense, when Duration multiplier has already been established and network steadies around a sable average quality multiplier, then it is true duration multiplier just cancels between numerator and denominator. There are however more subtle non-equilibrium effects, where the change in the duration multiplier will lead to different circulating supply dynamics that affect ROI, as network reaches equilibrium. The simulations CEL and Starboard are working on examine these effects. On the assumptions of raw power growth mainly let’s agree to disagree. Let’s examine and follow your scenario. I know it has become popular to say this FIP will turn Filecoin from PoW to PoS, but it Is not true in the sense that you don’t get higher multiplier simply because you locked higher collateral, you get it because you are on the hook for a longer time commitment, which involves more risk as well as more value to the network. Sealing 3 sectors for 1 year vs sealing 1 sector for 3 years: the first option has the benefit that you are free to do this for one year and then abandon the network, while the second option keeps you on the hook for longer, which the network values therefore rewards. But say following your assumption that all the SP’s decide it makes more sense to seal their sectors for 3 years. If that is the case, then 3 years simply becomes the new normal, as the average network quality multiplier is now 3. So the SP will get the same return on their one sector as before, just that the network standard has now become 3 years long. So if everyone had chosen to do 3 years, they still need to seal the three sectors if they want to have the previous ROI. What I’m saying is, if everyone decides to to seal a certain amount of time, that just becomes the new normal, if you want to keep your 3 sector’s worth of reward, you need to seal your 3 sectors, so I disagree with you on there existing this incentive for everyone to seal fewer sectors. If anything there exists an incentive to raise the average duration of a sector in the network. |

Beta Was this translation helpful? Give feedback.

-

|

@AxCortesCubero I don't want to be rude but I might need to ask you to stop putting words in my mouth, as I never concluded anything by misleading the community to believe my assumptions are facts, as you repeatedly implied. All I wrote in my opening and I quote here - Now back to the model,

|

Beta Was this translation helpful? Give feedback.

-

Filecoin Network Macro Commentary

|

Beta Was this translation helpful? Give feedback.

-

|

Did you see the initial pledge per TiB is increasing? As a provider, one would prefer sector extension to on-boarding new sectors from the cost perspective. In other words, the provider who does not want sector extension, will not onboard new sectors. In this case, what do we lose? |

Beta Was this translation helpful? Give feedback.

-

|

Thank you for the less technical writeup @zixuanzh!! Sincerely appreciated!!

Would you be able to expand on this point, please? This implies that the SPs who own these expiring sectors will not be using the released collateral to re-pledge new sectors. Are you able to share any modelling or data that supports this? Additionally, this FIP would potentially lead to a requirement of up to 5X the collateral pledge for the same 1X quantity of onboarded data. Won't this only serve to exacerbate the issue? Many thanks for your time! 🙏 |

Beta Was this translation helpful? Give feedback.

-

|

thanks for the filecoin macro overview, @zixuanzh - it's helpful to have the broader perspective in mind wrt timing of this particular FIP. @TippyFlitsUK to answer the question you have - I think for some SPs that I have talked to, there are harder aspects of the around working with investors / lenders (where the return needs to come faster, or the loan duration is only for 6 months to a year). so in that case the released collateral may have to go to pay back loans / investors etc. If the SP does not have enough capital/FIL themselves to continue operations, then that scenario would happen. I personally don't have a very deep understanding of the breakdown of SPs, but I do think a nontrivial percentage of them fall into this category. |

Beta Was this translation helpful? Give feedback.

-

|

Many thanks, @brendalee! It's great to hear feedback from as many SPs as possible and to learn about the various different challenges that we are all facing. This information has been rather lacking until this point so I really appreciate you sharing your findings!! It does sound like this regrettable outcome is already rather inevitable though. It's tough to see how this FIP will improve their circumstances within the time frames of concerning expiry that ZX has highlighted in his post. |

Beta Was this translation helpful? Give feedback.

-

|

@zixuanzh I very much appreciate your write up and elevating the conversation to the good of the whole ecosystem. I do want to dig a bit deeper into your statement I think there is a very important distinction to be made regarding growth of The key metric for our health needs to be growth of deal data onboarded (and yes longer deal durations are critical). It would make more sense for this FIP to encourage data onboarding and reduce incentives for CC growth. |

Beta Was this translation helpful? Give feedback.

-

|

If PL and FF had generated meaningful demand for the product through functionality, stability and customer engagement then we would not have this problem. Fixing circulating supply issue artificially through market manipulation at the expense of SP's is not the solution. The only winners here are those holding massive amounts of FIL, the Filecoin Foundation, Protocol Labs and their direct investors. If PL was not selling down / distributing their massive interest in FIL then perhaps the price would have held up a little better before today. |

Beta Was this translation helpful? Give feedback.

-

|

There's a ton of work that's being done around functionality / stability / customer engagement as @jnthnvctr has mentioned in the second half of his comment: #421 (reply in thread) . I think theres the reality of the time it takes to build a protocol / tooling / products within a short period of time (and just like any other engineering org, shipping faster also means that we have to resolve tech debt later on) and other factors outside our control (like the market environment). I think mentioned multiple times though, one of the goals of this FIP is to award the general Filecoin ecosystem - I do acknowledge there are realities that makes it difficult to realize these benefits depending on the situation though, many of which are detailed in the comments in this discussion. I think it would be helpful if you can share from your perspective how you wouldn't be able to benefit from different components of this FIP (which might not have already been pointed out), since the biggest motivation of the FIP was to reward participants in the network who have a longer term commitment. |

Beta Was this translation helpful? Give feedback.

-

|

The support for this FIP will come down to how it will be deployed day 1 and the clarity of goals/ outcomes. |

Beta Was this translation helpful? Give feedback.

-

|

It's been a long time since we had such a lively debate. |

Beta Was this translation helpful? Give feedback.

-

|

After the great infrastructural leap forward, the secondary market has seen a large number of equipment sold off. The current market conditions are such that every de-encapsulation of physical data is essentially an increase in fixed expenditure. There is a situation where the more you encapsulate, the more you lose. For every 1TB of data encapsulated, there are electricity costs, maintenance costs and software maintenance costs. This is a calculation that is better than not expanding in size. However, by retaining the current scale, we are unable to expand our profitability fundamentals. It is a game dilemma. The launch of FIP-421 breaks the current dilemma. Effective combination of capital flexibility and stockpiling of assets is utilised. Realised performance of SP on ecologically bullish long-term options while adjusting for secondary market idle capital. Lay the foundation for long term development of FIL Eco. We are in favor of this FIP |

Beta Was this translation helpful? Give feedback.

-

|

It's a very weak move, trying to use an economic method to cover the failure of building ecology/applications. Filecoin fails to attract clients/users to onboard their data onto mainnet. That's the reason why sectors growth is sluggish. The only way to solve this problem is to give more effort/reward to build the ecology, a popular application will be much more impactful to FIL price than a Ponzi FIP. TBH, even at this price, SP can still make a profit if sealing 100% FIL+ deals. SPs who spend too much on sealing machines and can not seal FIL+ deals are suffering. Those SPs are not here to provide storage service but make quick money, and they are leaving. That's not a bad thing for the community in the long run. Also, a 5-year pledge from now ensures Filecoin foundation and PL buyers of unfinished products. It won't be good stimulation for these 15% FIL holders who are also the main contributor. Onboard FVM, build applications and attract more users, that's what we should do. |

Beta Was this translation helpful? Give feedback.

-

|

I think @jnthnvctr said it well above:

Thousands of developers and hundreds of projects are, in fact, racing to build out valuable, real-world business models on top of Filecoin. This takes time, however, and requires trust in the stability of resources and infrastructure, which is what this FIP aims to accomplish. By comparison, AWS, Google Cloud, Azure, and Ethereum have had 16, 14, 12, and 7 years respectively to grow their ecosystems to where they are today. Filecoin has been working at it for 2, and has made pretty incredible progress in that short a time from my perspective. And regarding the inflammatory use of the term ponzi scheme, that is patently false. The tokens that Protocol Labs and Filecoin Foundation have are not some get-rich-quick scheme, but rather are being judiciously and amply put to work as salaries, grants, prizes, and startup investments towards building the ecosystem exactly as you suggest. |

Beta Was this translation helpful? Give feedback.

-

|

I'm pretty impressed by what PL and Fil Foundation have done, and I'm not intending to push them to do it faster. However, this FIP is not like what they used to do. Trying to use economic methods to limit the circulating supply is like a ponzi scheme for me. We have a better way, and we are working on it. And another reason why the QAP is not growing fast right now is that CC sealing overheated last year. A low-profit reality will force SPs to choose more cost-efficient solutions and participant in high-value projects (like Fil+, slingshot). As you can see, the proportion of verified data grows faster and faster. I think we are heading in the right direction without this Fip. |

Beta Was this translation helpful? Give feedback.

-

|

@mogli0528 I consider a lot of the feedback raised in this discussion to be constructive and points out the other pain points & things that should be considered to be prioritized by the team working on making Filecoin better (including your comments). Many of them should be broken into their own FIP discussion and be in community & core dev's backlogs.